What Is Selling Price At Specified Service Business

Executive Summary

While much of the Tax Cuts and Jobs Human action of 2017 was focused on individual and corporate revenue enhancement reform and simplification, i of the biggest new planning opportunities that emerged was the creation of a new twenty% taxation deduction for "Qualified Business concern Income" (QBI) of a pass-through entity, intended to provide a taxation benefaction to small businesses that would leave more than profits with the business organisation to help it grow and hire.

The caveat, however, is that the QBI deduction was merely intended to provide taxation benefits for assisting businesses that rent employees, not to provide tax benefits for high-income professions who generate their profits directly from their own personal labors. Every bit a issue, the new IRC Section 199A created a and so-called "Specified Service Concern" nomenclature that, at higher income levels, would not be eligible for the QBI deduction.

The challenge, however, is that the exact definition of what constitutes a "Specified Service Merchandise or Business" (SSTB) has not always clear, given the broad range of professional services that exist in the market. In addition, every bit soon equally the rules themselves were released, creative tax planners began to strategize almost how to conform (or re-arrange) revenue and profits to maximize the amount of income eligible for the QBI deduction and minimize exposure to the Specified Service Business rules.

In this invitee post, Jeffrey Levine of BluePrint Wealth Alliance, and our Director of Counselor Education for Kitces.com, examines the latest IRS Proposed Regulations for Section 199A, which provides both of import clarity to how the "Specified Service Business organisation" exam will apply in various industries, including rather broadly for professions like wellness, law, and accounting, but only narrowly to high-profile celebrities who may have their endorsements and paid appearances treated as specified service income just not the income from their other businesses that may still materially benefit from their loftier-profile reputation.

Of greater significance for many small business owners, though, are new rules that will force businesses with even only modest specified service income to treat the entire entity equally an SSTB, limit the power of specified service businesses to "carve off" their non-SSTB income into a separate entity, and in many cases amass together multiple commonly owned SSTB and not-SSTB business organization for tax purposes.

Ultimately, the new rules are simply impactful for the subset of pocket-size business owners who engage in specified service business organization activities and take enough taxable income to exceed the thresholds where the phaseout of the QBI deduction begins (which is $157,500 for individuals and $315,000 for married couples). Nonetheless, for that subset of high-income business owners, effective planning to avoid having SSTBs "taint" not-SSTB income, or to split off non-SSTB income to the extent possible, will be more challenging than before.

IRS Issues Proposed Regulations ane.199A On The Qualified Business Income Deduction

On August viii, 2018, the IRS released the much-anticipated proposed regulations for IRC Section 199A. The regulations provide a veritable treasure-trove of information, and in detail, articulate up many of the questions surrounding Specified Service Trade or Businesses (SSTB). Most importantly, they provide much-needed clarity to decide exactly what businesses should be classified every bit an SSTB (or not). This determination is of minimal importance to low and moderate income earners (upwardly to $315,000 for married couples filing joint returns, and up to $157,500 for all other filers), but is critical to high earners above those thresholds, who may see their qualified business income (QBI) deductions related to specified service trade or businesses partially or fully phased out as their income exceeds those thresholds.

Understanding The Definition Of A Specified Service Trade Or Business organization (SSTB)

The primary purpose of the IRC Department 199A deduction for Qualified Business Income (QBI) was to provide a tax boon for businesses that hire and utilize people to grow the US economy, but not to requite a deduction to those who simply earned a substantial income from the fruits of their ain labor. Not that all service businesses would be prohibited… just specifically the ones that generated income primarily past providing various types of professional services.

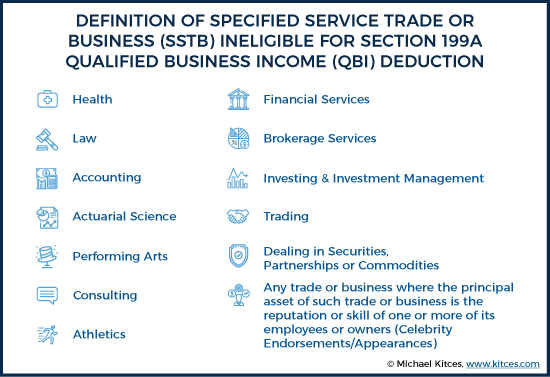

Appropriately, IRC Department 199A defines sure "SpecifiedService Merchandise or Businesses" (SSTBs) that, at college income levels, are not eligible for the QBI deduction. Cartoon on IRC Section 1202(east)(3)(A) (which defines eligibility for certain types of small business stock capital letter gains to be excluded from income, and similarly is not bachelor for professional person services firms), the legislative text of IRC Section 199A stipulated that an SSTB would include:

"…whatsoever trade or business involving the performance of services in the fields of health, police force, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or whatever trade or business concern where the primary asset of such trade or business is the reputation or skill of 1 or more of its employees."

(Notably, IRC Section 1202(east)(3)(A) too includes engineers and architects, simply those professions were explicitly excluded from the list of SSTB professions nether IRC Section 199A(d)(ii)(A).)

In addition to the businesses listed to a higher place, IRC Section 199A(d)(2)(B) adds the post-obit businesses to the list of SSTBs:

"…any trade or business concern which involves the performance of services that consist of investing and investment management, trading, or dealing in securities."

While some of these professions are relatively straightforward to define, the original legislative text for Section 199A left much up to interpretation when determining whether or not certain businesses would be treated as a specified service trade or business (SSTB), both with respect to certain border cases inside professions (due east.1000., does an accountant who only does tax preparation merely not business accounting and auditing yet "count" as accounting services, and does income from selling insurance products count equally "financial services" or only providing investment communication?), and the relatively broad grab-all at the end of the SSTB list for "whatever trade or concern where the principal nugget of such trade or business is the reputation or skill of one or more of its employees" (raising the question of whether a restaurant qualifies for the QBI deduction, simply a eating place with a star chef might not?).

Clarifying The Telescopic Of Professions That Are "Specified" Service Businesses

Fortunately, the new IRC Section 199A regulations provide a groovy deal of clarity almost where, exactly, to draw the line between the 13 different types of specified service businesses and all other types of service businesses.

Some types of SSTBs are relatively straightforward and required minimal clarification from the IRS, such as athletics and performing arts. The regulations practice, however, clarify that persons engaged in supporting services, such every bit those who maintain or operate equipment or facilities for such businesses, are not SSTBs, themselves.

Determining what types of and roles inside various professional person service occupations fall into – and only as of import, practise not fall into – the other SSTB categories was less clear from the original legislation, though, and thus required more than specific guidance from the IRS in the regulations.

Health, Law, and Bookkeeping Services Are Divers Broadly For Specified Service Trade Or Business

Given that the healthcare sector is now the largest employer in the Us economy, "Health" services was i area where there were a number of open questions about the telescopic of the specified service rules. For example, while information technology's relatively straightforward that doctors are in the wellness profession… information technology was less clear whether pharmacists and similar 'related' healthcare professionals would be included in the definition, also as veterinarians and others providing "healthcare" to not-humans. The proposed regulations accept an inclusive approach here and brand articulate that both pharmacists and veterinarians are considered health services, and thus, are SSTBs. Accordingly, the newly proposed regulations stipulate that:

"…the performance of services in the field of health means the provision of medical services past individuals such equally physicians, pharmacists, nurses, dentists, veterinarians, concrete therapists, psychologists and other similar healthcare professionals performing services in their capacity as such who provide medical services directly to a patient (service recipient)."

The proposed regulations also have a similarly inclusive arroyo with respect to the fields of "accounting" and "law." As a result, the quondam includes not just "accountants," but also "enrolled agents, return preparers, financial auditors, and similar professionals," while the latter also includes "paralegals, legal arbitrators, mediators, and like professionals" in addition to lawyers, themselves.

Not All Financial Services Are Treated As SSTB Financial Services

Of detail importance to fiscal professionals, v of the 13categories of SSTBs directly relate to various professions inside the fiscal manufacture (fiscal services, brokerage services, investing and investment management, trading and dealing in securities, partnerships or commodities), while two more could relate indirectly (consulting and the "principal asset is the skill or reputation of one or more employees"). Thus, many loftier-income owners of fiscal services businesses will be considered owners of an SSTB and will brainstorm to see their QBI deduction stage out in one case their income exceeds their applicable threshold.

Some of the financial services professions explicitly "called out" in the proposed regulations equally unequivocally being SSTBs include "financial advisors, investment bankers, wealth planners, and retirement advisors," as well as those "receiving fees for investing, asset direction, or investment management services, including providing advice with respect to buying and selling investments." Businesses engaged in either the trading or dealing of securities, commodities, or partnership interests are also SSTBs, every bit are brokers of securities (i.e., registered representatives of a broker-dealer).

While virtually financial services professionals are engaged in SSTBs, the regulations practise exclude real estate agents and brokers from the definition of an SSTB as well. More importantly, though, the regulations as well grant 2 other very notable exceptions to the rule: traditional bankers (not investment bankers), and insurance agents or brokers. Is this merely because they have meliorate lobbyists than the balance of the financial manufacture? Possibly that played at to the lowest degree some role, but the crux of the upshot can be traced back to the initial legislative text creating the QBI deduction.

As noted earlier, under IRC Section 199A(d)(ii)(A), an SSTB is any business described in IRC Department 1202(e)(3)(A), other than engineers and architects (who apparently also have very good lobbyists!), including:

"…whatever trade or business involving the functioning of services in the fields of wellness, police force, accounting, actuarial scientific discipline, performing arts, consulting, athletics, fiscal services, brokerage services, or any trade or business concern where the principal asset of such trade or business is the reputation or skill of 1 or more of its employees."

Conspicuously absent-minded from the list of businesses above are banking and insurance. Notably, these businesses are included in the following subparagraph of the IRC, IRC Section 1202(east)(three)(B), which states:

"any banking, insurance, financing, leasing, investing, or similar business"

However, when Congress wrote the law defining what constitutes an SSTB, it explicitly stated only the professions under IRC Section 1202(e)(three)(A) – and not IRC Section 1202(e)(three)(B) – would count. Accordingly, the IRS determined in its proposed regulations that a more than narrow interpretation of "fiscal services" (1 that does non include traditional banking or insurance services) was appropriate. After all, if Congress wanted to include those businesses in the definition of SSTBs, they could have referenced both IRC Section 1202(e)(3)(A) and IRC Section 1202(e)(3)(B) when it created IRC Section 199A. Its failure to do so provided the IRS with enough legislative intent that they explicitly excluded those businesses from the definition of an SSTB in the regulations.

Equally a result of the difference between the manner qualified business income from financial planning/securities brokerage/investment advice is treated as compared to qualified business income from insurance services, many registered investment advisors and/or securities brokers who also conduct insurance business organisation will discover that the profits from their different businesses will be treated markedly different from one another. While profits from the financial planning/securities brokerage/investment advice concern(es) will exist potentially ineligible for the QBI deduction one time the owner's taxable income exceeds $207,500, or $415,000 if married and filing a joint return, profits from the insurance business may still eligible for the deduction as a non-SSTB (though calculating the deduction would notwithstanding involve analyzing the West-2 wages paid past the insurance business, as well every bit whatever depreciable property owned by the business, nether the separate wage-and-holding examination for the QBI deduction).

Unfortunately, though, it is not uncommon for certain advisors, particularly solo-advisors, to run both their brokerage/advisory acquirement and their insurance revenue through the same "financial counselor" sole-proprietorship. In the past, this often made sense, as treating the brokerage/advisory business every bit a carve up business from the insurance-related business would generally lead to unnecessary complexity and expense, both from the requirement to go along two sets of books, every bit well every bit the demand to file multiple Grade Schedule Cs (or other business returns) with the counselor's personal income revenue enhancement return.

At present, however, in lite of the proposed regulations' differentiation between the profits of the two businesses, loftier-income advisors may wish to more clearly dissever and delineate these different "lines of business" into ii, distinct businesses. If non, the proposed regulations' de minimis rule, discussed in greater depth beneath, could "taint" whatsoever insurance services profits that would otherwise be eligible for the QBI deduction.

When the legislative text for IRC Department 199A was created, i of the most nebulous aspects of the definition of an SSTB was the catch-all provision that, "whatsoever trade or business organisation where the main nugget of such trade or business organization is the reputation or skill of 1 or more of its employees," is an SSTB. How would the IRS make up one's mind whether an employee or business owner's "skill or reputation" was the driving force behind the business organization'south profits? Rightfully so, many practitioners were concerned that this language could ensnare simply about any business with a successful and high-profile founder/owner.

For example, "Jan's Article of furniture Shop" probably doesn't fall into the category of an SSTB. But what if Jan was highly regarded as the most skilled furniture maker in town, and her reputation every bit a skilled craftsman was what drove sales? Exactly how skilled or respected would Jan accept to exist before the business organization crossed over from a non-SSTB to an SSTB? Similarly, "Bob'southward Diner" probably isn't an SSTB, but what if "Bob" was really famous chef Bobby Flay? Clearly, such an analysis is highly subjective at best, which was a principal driver of many practitioners' concerns.

Thankfully, these concerns are no longer necessary. In what was a relatively surprising motion, the IRS defined the meaning of a trade or business organization where the main asset of that business is the reputation or skill of one or more employees or owners in, perhaps, the narrowest of possible ways.

Co-ordinate to the proposed regulations, a business is only considered an SSTB by virtue of the "reputation or skill" provision if, and only if, it generates fees, compensation, or other income via one or more than of the post-obit:

- Endorsements of products or services;

- Utilise of an individual's image, likeness, proper noun, signature, vocalization, trademark, or any other symbol associated with the individual's identity;

- Appearances on radio, tv, or other media.

As a effect of the IRS'south extremely narrow estimation of the "reputation or skill" provision in the 199A regulations, the provision has gone from potentially being one of the chief culprits of classifying a business as an SSTB, to being fairly beneficial, and applicable but to an extremely limited number of "businesses" that are truly congenital around "celebrity" endorsements, appearances, and the like.

In fact, the proposed regulations include a number of IRS-provided examples, and Example 8 of Section 199A-5(b)(three) of the regulations provide perhaps the best insight as to how narrowly the IRS has framed this "reputation or skill" provision.

H is a well-known chef and the sole owner of multiple restaurants, each of which is owned in a overlooked entity. Due to H's skill and reputation as a chef, H receives an endorsement fee of $500,000 for the use of H'due south name on a line of cooking utensils and cookware. H is in the trade or business organization of being a chef, and owning restaurants and such merchandise or business organization is not an SSTB. However, H is also in the merchandise or business of receiving endorsement income. H's merchandise or business consisting of the receipt of the endorsement fee for H's skill and/or reputation is an SSTB within the meaning of paragraphs (b)(1)(xiii) and (b)(2)(14) of this section.

If the chef in the instance above is able to receive an endorsement fee of $500,000 for the apply of their name on a line of cooking utensils and cookware, it's probably pretty safe to assume that they are not simply a pretty good chef (i.e., they are skilled) but that they are too adequately well known (i.eastward., has a potent reputation). As such, two of the principal drivers of the chef's restaurants revenues are probable the chef's skill and reputation. And all the same, in the example, the IRS makes clear that these restaurants would non be considered SSTBs, as they do not see the (favorably) rigid definition of the "reputation or skill" provision outlined higher up, despite the fact that they are probable successful at least in material part to the "reputation or skill" of their glory chef-owner.

Many businesses engage in more than 1 specific activity or business line at a time, creating a potential claiming to determine whether or non the business organization, as a whole, is an SSTB. In some cases, this is ostensibly easier because the business lines are literally separated into unimposing divide entities, for liability protection and/or other purposes (even though they're still "related" entities). Though in the extreme, separating businesses into discrete entities as well creates the concerning potential (at least for the IRS) that firms volition cleave off what otherwise would accept been SSTB profits (not eligible for the QBI deduction) into split entities that would qualify (even though in the aggregate it shouldn't have).

Appropriately, the proposed regulations provide guidance on how to bargain with both circumstances, both with respect to determining when the SSTB revenue in an otherwise non-SSTB business must exist treated equally such, and when and whether to aggregate dorsum together split up-but-related SSTB and non-SSTB entities into one SSTB.

Application of the "De Minimis Rule" In Determining A Specified Service Trade or Concern

Oftentimes, a single business will simultaneously conduct multiple business activities. In some situations, one or more than of those detached activities, if conducted by a separate business, would cause that business to be treated equally an SSTB. The proposed regulations practise not, as some had hoped, allow a unmarried business to separately business relationship for different lines of revenue and expenses and segregate SSTB profits vs. non-SSTB profits. Instead, the unabridged business is either an SSTB… or it's not. Every bit such, either all of the profits of a business are profits of an SSTB entity, or all of the profits are profits of a non-SSTB.

This raises an obvious question… how much revenue can a unmarried business generate from an activity that would be considered an SSTB if conducted in its own, separate business, before the entire business is considered an SSTB? The answer, unfortunately, is "not much."

Under the proposed regulations, if a business has gross acquirement of $25 1000000 or less during a taxable yr, then the business must keep its SSTB-related revenues to less than ten% of its gross revenue to avoid SSTB condition. Or conversely, the $25M-or-less-revenue concern will be considered an SSTB if only 10% or more than of its gross revenue is derived from an SSTB-blazon activity!

In the event a business generates more than $25 million of revenue during a taxable yr, the SSTB rules are fifty-fifty more than restrictive. Such businesses will be considered an SSTB if but 5% or more of their gross acquirement is derived from an SSTB-related activity.

Example #one: Frank is an optometrist, and is the sole owner of Spectacular Spectacles, LLC, which is primarily engaged in the manufacturing and sale of eyeglasses (non an SSTB-related activity). Occasionally, however, Frank will perform (and charge for) heart examinations, in function, to determine a customer's right prescription. These exams are related to health services, and thus, are an SSTB-related activity.

In 2018, Spectacular Spectacles, LLC generates $3 1000000 of gross revenue. The $3 1000000 of gross acquirement is comprised of $2,880,000 million of acquirement related to the manufacturing and sales of eyeglasses, with the remaining $120,000 of acquirement attributable to Frank's occasional vision exams. Since just iv% ($120,000 / $three meg = iv%) of Spectacular Spectacles, LLC'southward full revenue is comprised of SSTB-related revenue, the business will not be considered an SSTB.

Specified Service Revenue Taints Non-SSTBs And The Incidental SSTB Dominion

There are a number of interesting corollaries to the SSTB de minimis rule. Most notable is the fact that although it's business's profits that are eligible for the QBI deduction in the first place, the determination of whether or not a concern with revenue from multiple activities is considered an SSTB is determined solely past the ratio of its revenue from SSTB activities in relation to its full revenue. Which is concerning, considering it means a high-revenue depression-margin specified service concern can taint the QBI deduction for an entire high-turn a profit non-SSTB!

Instance #2: Bill, i of Spectacular Spectacles, LLC's employees, decides to go out and offset his ain eyeglass manufacturing and sales visitor, Spectacles for the Masses, LLC. Pecker is not a physician, simply in an try to bulldoze business concern and compete with his former employer, he hires several optometrists who can perform vision examinations and heavily promotes and advertises this service.

In 2018, Glasses for the Masses, LLC generates $1.6 million of revenue and $550,000 of profits. Equally a issue of the profits, Bill is over his applicable threshold, and thus, will be ineligible for any QBI deduction if his business concern is deemed an SSTB.

Analyzing Glasses for the Masses, LLC's revenue and profits farther, information technology is adamant that $400,000 of the company'due south total acquirement is derived from the heavily marketed eye examinations. However, later accounting for expenses, including the salaries of the two optometrists, this activity only generates $50,000 of profit. In dissimilarity, the cadre concern of manufacturing and selling eyeglasses generates $1.ii million of revenue, and $500,000 of turn a profit.

Simply virtually 9% ($fifty,000 /$550,000 = 9.09%) of Spectacles for the Masses, LLCs profits are owing to an SSTB-related activity. The entire business organisation, nonetheless, and all of the profits, volition be considered an SSTB for 2018 since 25% ($400,000 / $1.6 one thousand thousand = 25%) of its revenues are attributable to the SSTB-related optometry activity… well more the 10%-of-acquirement hurdle necessary to wind up with that categorization. The stop result? Bill gets $0 of QBI deduction on his $550,000 of profit (almost all of which was non-SSTB profit, just all of which was disqualified equally a high-income SSTB business however!).

For concern owners like Neb, there are a couple of different options.

I option, for instance, would be to merely eliminate the SSTB-related action that's not all that profitable in the first place. Unfortunately, that may be easier said than done. What if much of Glasses for the Masses, LLC's revenue and profits from the manufacturing and auction of spectacles (non-SSTB-related) is due to the fact that customers are able to get an eye examination and buy their eyeglasses in 1 location (which, in the extreme, could arrive worthwhile to continue the SSTB service that disqualifies the QBI deduction simply considering it'south "necessary" for the business)?

Another option for business concern owners like Bill is to carve up the various activities into legitimate, bona fide, split up businesses. In such situations, each business will mostly be evaluated on its ain merits. Splitting activities into split businesses in this manner (east.1000. creating GM Optometry to perform optometry services) might create some operational challenges for Bill, such every bit the need for customers getting an center exam and purchasing glasses to pay two dissever bills to the two separate companies (an centre exam bill to the optometry business organization and a spectacles bill to Glasses for the Masses, LLC), but the resulting revenue enhancement benefits may be worth information technology. In Beak's example, it would mean a 20% revenue enhancement deduction on upwardly to $500,000 of profits… annually!

On the other hand, the proposed regulations do take an boosted layer of rules specifically intended to limit splitting off a multitude of pocket-size not-SSTBs to insulate them from an SSTB core (which wouldn't be applicable in the case higher up, but could be an issue for an optometrist that primarily provided center exams as health services and just sold a few eyeglasses "on the side"). Specifically, nether the "incidental-to-SSTB" rules, if a non-SSTB has 50%-or-more common ownership with an SSTB and has shared expenses, it must have revenues of more than than 5% of the combined revenues of both businesses, or they will all exist aggregated as an SSTB anyway. Appropriately, in order to be treated every bit a separate SSTB (and non taint the not-SSTB core), the separate business must either have revenues of more than 5% of the combined entities, or have its own entirely contained cost construction and non share wages, overhead, or other business expenses.

Example #3: Jerry, Spectacular Spectacles, LLC'south virtually pop optometrist, decides to get out on his own as an optometrist, and over 3 years quickly grows to generate $500,000/year of revenue. While Jerry's business is solely focused on providing optometry (health services), which is an SSTB, his married woman Elaine (an creative person) suggests that he start selling a small number of designer eyeglasses (with her fine art designs).

After 2 more years, Jerry'southward optometry practice grows to $600,000/twelvemonth in revenue, and his wife'south carve up eyeglass business (sold in Jerry's medical offices) generates $15,000 of revenue. Normally, an eyeglasses business is not an SSTB, but considering Elaine's eyeglass business is under mutual ownership with Jerry's optometry concern (via the shared attribution rules for married couples), and they share expenses (since she uses Jerry's part infinite to sell her glasses), and the eyeglass revenue is only 2.iv% of the combined $xv,000 + $600,000 = $615,000 revenue, whatsoever profits on Elaine'due south eyeglass business will exist treated as SSTB income (phasing out their QBI deduction altogether given Jerry'south high income).

Further complicating the matter is the fact that a concern conducting both SSTB-related and non-SSTB-related activities may periodically change from an SSTB to a non-SSTB (or vice versa), and dorsum once more, depending upon the ratio of SSTB-related acquirement to total revenue each year.

This is possible because, nether the proposed regulations, the de minimis dominion states that:

"For a merchandise or concern with gross receipts of $25 1000000 dollars or less for the taxable year , a trade or business organisation is non an SSTB if less than 10 per centum of the gross receipts of the trade or business organization are owing to [an SSTB]". (accent added)

The key point is that the proposed regulations' stipulate that the de minimis rule is applied separately "each taxable year." As a result, the conclusion of whether a business conducting both SSTB-related and non-SSTB-related activities is itself an SSTB is an annual test, based on whether the SSTB-related revenue is more than 10% (or in the case of >$25M revenue businesses, more 5%) in each yr!

The 80/l "Spin-off Killer" Rule (A.K.A. The Anti- "Crack and Pack")

Most immediately afterward the Revenue enhancement Cuts and Jobs Act's cosmos of IRC Section 199A, practitioners went to work dissecting the new section and coming upwards with creative means to let clients to claim greater deductions.

One of the about widely discussed strategies for loftier-income business organization owners was something that came to be known every bit the "crack and pack." In brusque, the "crack and pack" was simply the thought of spinning off certain elements of an SSTB – oft business organization-endemic real estate - into a separate, commonly-owned entity, in guild to shift income from an SSTB (for which a QBI deduction on profits may have been phased out) to a non-SSTB (for which a QBI deduction on profits may still exist available).

Unfortunately, the proposed regulations put a severe contraction – if non a death knell – in the "crevice and pack," thanks to the new "80/50 rule" outlined in Department 199A-5(c)(2) of the regulations.

Nether this provision, if a "non-SSTB" has l% or more common buying with an SSTB, and the "non-SSTB" provides 80% or more of its property or services to the SSTB, the "non-SSTB" will, by regulation, be treated as role of the SSTB.

Example #4: Betty is a doctor, and is the sole possessor of her practice, which is organized as an LLC. The internet income from her practice – which falls under the "health" services category of the SSTB definition – is $800,000 per year. Equally a result, Betty cannot claim a QBI deduction. Betty'southward LLC also owns the medical part out of which she practices, having purchased it several years ago for $2,000,000.

Prior to the issuance of the proposed regulations, one strategy Betty might have contemplated with her tax planner was spinning the medical office out into a separate LLC, or other business construction, and having the medical practice pay rent to the rental business for its utilize of the property. Prevailing wisdom was that while the profits of the medical practice would accept been ineligible for the QBI deduction, the profits from at least the new (now-separate) rental business would have eligible for at least a partial QBI deduction (effectively converting that portion of the income from SSTB to not-SSTB income).

The proposed regulations make clear that such a series of transactions would at present be fruitless. Bold that Betty's medical practice continued to use 100% of the office space after information technology was spun out into a new entity, she would be in "violation" of the "80" part of the eighty/fifty dominion, since more lxxx% of the non-SSTB's belongings would be used past a SSTB. Similarly, assuming she was the owner of the business into which the medical office was transferred, she would exist in violation of the "fifty" part of the fourscore/50 dominion, since the mutual ownership betwixt the SSTB and the not-SSTB would exist 100%! Thus, the rental business concern and its income would, past rule, still be treated every bit an SSTB.

The "best" way to "crush" the 80/50 rule will often be to "attack" the "50" part of the dominion by trying to get the common buying between the SSTB and the not-SSTB business entities below 50%. Once the common ownership (which includes both direct and indirect ownership by related parties) between the 2 entities is less than fifty%, the anti-"crack and pack" rules don't apply, and the not-SSTB will actually be treated every bit a non-SSTB!

Notably, trying to avoid the eighty/50 dominion by but ensuring the SSTB business uses less than 80% of the non-SSTB'south property and services (e.m., by buying the entire medical office complex, renting out the other suites, and using only a minor portion of the office space for the ordinarily owned medical practice) will only be of limited effectiveness. The reason is that, nether the rules, if a "non-SSTB" is providing less than eighty% of its services/property to a 50%-or-greater ordinarily-owned SSTB, a portion of the business's profits will still exist considered role of an SSTB! In such situations, the portion of the business organisation'southward services/property that is not provided to the unremarkably-owned SSTB will not be treated every bit an SSTB, but the portion of business'south services/property that is provided by commonly-owned SSTB will still exist treated as an SSTB!

Example #5: Kanwe Beatum, LLC, is a law firm, and thus, an SSTB. The owners of the firm take recently decided to purchase a large role building in a separate (but commonly owned) entity, Fancy Offices, LLC, of which 40% volition be rented to Kanwe Beatum at off-white market value to bear future operations, while the other lx% volition exist rented to unrelated businesses.

Hither, only 40% of the non-SSTB Fancy Offices property (the building) will be provided to the SSTB law house (which is lower than the 80% threshold). The buying, notwithstanding, between Kanwe Beatum, LLC and the Fancy Offices entity in which the office edifice is purchased is identical (≥fifty%). As a result, forty% of Fancy Offices will be treated as an SSTB (i.east., xl% of its revenue and profits will be subject to the SSTB phaseout tests), while the remaining sixty% will not.

Ultimately, the "expert" news of the new SSTB rules is that they nevertheless only utilise to a limited subset of small business owners – those that practice engage in at least some level of "specified services", and take income that is high enough to exceed the thresholds ($157,500 for individuals and $315,000 for married couples) where the QBI phaseout kicks in. Nonetheless, for high-income small business organization owners who practise meet those thresholds and accept specified service income, conscientious planning will be more important than ever to avoid running afoul of the new rules, specially with respect to trying to separate (and avert "tainting") not-SSTB income from the less-tax-favored income of specified service businesses.

What Is Selling Price At Specified Service Business,

Source: https://www.kitces.com/blog/sstb-specified-service-business-de-minimis-rule-crack-and-pack-80-50-rule-qbi-deduction/

Posted by: warrengrep1973.blogspot.com

0 Response to "What Is Selling Price At Specified Service Business"

Post a Comment